Presentation of Covid-19 Related Federal Programs on the Schedule of Expenditures of Federal Awards

4/22/2021 - By Amy Guerra, CPA

New aid provided by federal agencies in response to the COVID-19 pandemic can impact the presentation of your organization’s Schedule of Expenditures of Federal Awards (SEFA), Notes to the SEFA, and Federal Audit Clearinghouse Data Collection Form (DCF). As you prepare for your audit, it is important to understand the funding you received and identify the COVID-19 related funds separately on the SEFA provided to the auditors to support an effective audit.

Various federal programs provided new aid in response to the COVID-19 pandemic. Certain funds are subject to single audit, which requires recipients to prepare an SEFA. Federal agencies may have incorporated COVID-19 funding into an existing program and CFDA number or established a new COVID-19 program with a unique CFDA number. Federal agencies are required to specifically identify COVID-19 awards, regardless of whether the funding was incorporated into an existing program or a new program.

If an entity receives COVID-19 funds and makes subawards, the information furnished to the subrecipients should distinguish the subawards of incremental COVID-19 funds from non-COVID-19 subawards existing under the program.

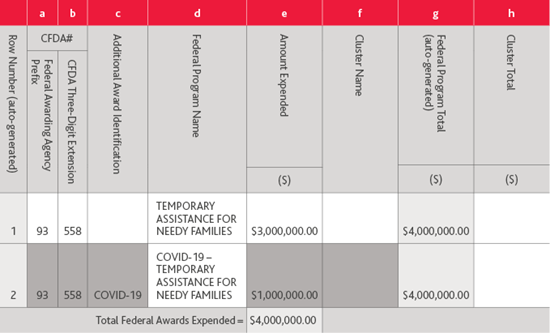

All COVID-19 funding is required to be identified as such per Appendix VII of the OMB 2020 Compliance Supplement (Supplement). To maximize the transparency and accountability of COVID-19 related award expenditures, non-federal entities should separately identify COVID-19 expenditures on the SEFA by presenting this funding on a separate line by CFDA number with “COVID-19” as a prefix to the program name. The following is an example of such presentation based on the OMB 2020 Compliance Supplement Appendix VII.

In addition to separately identifying COVID-19 expenditures on the SEFA, there are new disclosures related to COVID-19 assistance that needs to be incorporated in the notes to the SEFA. Federal sources may have donated personal protective equipment (PPE) to an organization for the COVID-19 response. Nonfederal entities that received this donated PPE should provide the fair market value at the time of receipt as a stand-alone footnote accompanying their SEFA. As the donated PPE does not impact the single audit, the stand-alone footnote may be marked as “unaudited.” PPE that is purchased using federal funds provided to the entity should be reported as federal expenditures.

The amount of donated PPE should not be counted for purposes of assessing whether your organization is over the $750,000 threshold of federal expenditures used to determine if a single audit is required. Donated PPE would also not count toward the Type A and Type B threshold for major program determination.

If a nonprofit organization is subject to single audit, it also requires a DCF submission to the Federal Audit Clearinghouse. At this time the instructions to the DCF have not been amended but entities should follow the OMB Compliance Supplement guidance to show the COVID-19 programs separately. The OMB Compliance Supplement recommends that the COVID funds should be entered on a separate row by CFDA number with “COVID-19” in the “Additional Award Identification” column. See example below:

As you prepare your internal SEFA be sure to follow this guidance.

If you have any questions, don't hesitate to reach out to our Non-Profit Team!

This article originally appeared in BDO USA, LLP's "Nonprofit Standard Newsletter" (Spring 2021). Copyright © 2021 BDO USA, LLP. All rights reserved. www.bdo.com

Related Posts

- Are there State Tax Liabilities for Employers if Employees Work from Home?

- Webinar Materials: Rethinking Financial Reporting - Nonprofit Strategy

- Webinar Materials: New Mortgage Servicing Rules

- Cryptocurrency - It's Time to Acknowledge the Elephant in the Room

- WEBINAR MATERIALS: PRF Reporting Update for Healthcare

- What's New with the Employee Retention Credit: An Overview

- White Paper: Manufacturing Outlook, Lean Thinking to Reduce Costs

- Higher Education in the U.S. - Rising Costs, Enrollment Challenges and the Need for Innovative Solutions

- WEBINAR MATERIALS: Current Update on CARES Act PRF Reporting Instructions & Recent FAQs

- 2021 State & Local Tax Year-End Issues to Consider Now

- The Sky Is Not Falling... Yet

- Cares Act vs American Rescue Plan Act Funding

- GovCon Updates of the Week Part 10

- Covid-19 Implications For Presumptive Laws And Workers' Compensation

- Asset Liability Management Modeling in a COVID-19 World

- Maximizing Value and Minimizing Risk in Your Managed Care Contract Portfolio

- The Excess Liquidity Puzzle

- Finding Flexibility Amid COVID-19: How Nonprofits Can Scale for Success

- White House Unveils Plan to Help American Families Funded by Tax Increases on Wealthy

- Tech Leaders Worldwide Have Optimistic Outlook For 2021

- White Paper: Manufacturing Outlook, Help Wanted

- Employer Tax Credit for Vaccine-Related Sick Leave

- GovCon Updates of the Week Part 5

- IRS Issues Guidance for Claiming Employee Retention Credit in 2021

- Five Metrics Your Construction Company Should Start Tracking Today

- View All Articles

{kind=link}